How to Build Customer Loyalty in the Insurance Industry: An 8-Step Guide

25 min to read

Published: February 8, 2023

Updated: July 17, 2026

Customer loyalty in the insurance industry is the degree to which policyholders choose, engage with, and advocate for a provider, driving customer retention and sustainable growth.

In a crowded market, loyalty protects margins, lifts customer lifetime value, and builds trust and reliability across digital channels when products feel interchangeable and price sensitivity rises.

Mark Camp

CEO & Founder at PropelloCloud.com

Contents

Key Takeaways

Building customer loyalty in insurance requires transparent pricing, exceptional service quality, and consistent trust-building across all touchpoints.

Strategic brand partnerships now form the foundation of successful loyalty programmes, with 86% of insurance companies investing in this area.

Data-driven personalisation has become a competitive necessity, with 84% of insurers prioritising tailored customer experiences.

Insurance companies face unique loyalty challenges, with 85% struggling with customer engagement and 80% with churn management.

The most effective loyalty strategies balance immediate benefits like cashback with long-term value through tiered memberships and experiential rewards.

Mobile-first engagement is essential, as 77% of businesses are investing in seamless digital experiences for customers.

This guide gives you a practical playbook for building customer loyalty in the insurance industry.

You will learn how to replace price wars with personalised experience, digital self-service, risk prevention, and loyalty programmes powered by data analytics so you cut churn and grow advocacy across every digital channel.

How Loyal Are Insurance Customers Right Now?

Not very. Industry data paints a stark picture of low trust, weak advocacy, and high switching intent across the sector.

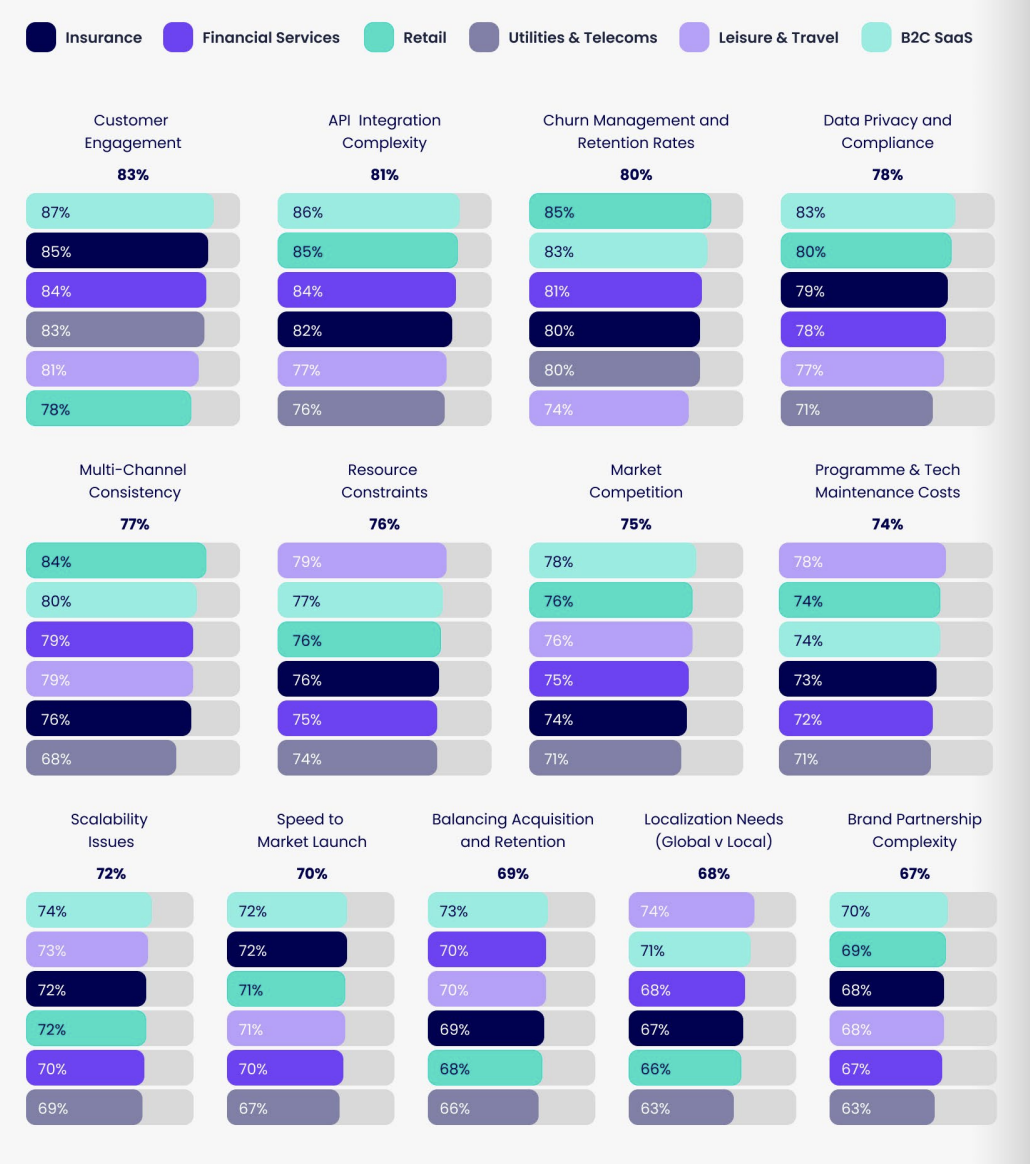

According to our 2025 Loyalty Uncovered Report, 83% of insurance businesses cite customer engagement as their top concern, with 37% rating it a critical challenge.

According to a 2022 Ello Group survey, just 8% of policyholders have remained faithful to their insurer for 3+ years, and only 13% trust their current provider.

Further research highlights fragile advocacy and switching intent, with J.D. Power’s auto insurance report revealing that only half of customers would recommend their providers.

According to a 2023 study, 37% of UK consumers said they would be open to switching auto insurance companies within the next 12 months, mostly in search of more affordable plans.

Let’s discuss the challenges that are driving these numbers.

What Are the Customer Loyalty Challenges Facing UK Insurers?

The major customer loyalty challenges facing UK insurers are:

Infrequent customer interactions

Declining trust, rising churn

Regulatory disruption

Digital-first expectations

Spiralling acquisition costs

Product commoditisation

Complex policies and claims processes

Evolving customer expectations

Legacy systems that prevent a unified experience

With roughly 40% of customers switching their home or vehicle insurance annually, the sector has one of the lowest retention rates of any industry. This should set alarm bells ringing when you consider that boosting retention by just 5% can increase profits by up to 95%.

Insurers offer huge discounts to new customers to draw them in, with loyal, existing customers paying significantly higher rates. This loyalty penalty, coupled with the lack of incentive to keep them around, is why customers choose to shop around rather than stay loyal.

Meanwhile, loyal customers are more likely to spend more, remain customers for longer, cut costs, and advocate for their service providers.

Our research indicates the top challenges facing the insurance industry, in comparison with other industries when it comes to achieving customer loyalty.

Customer engagement (85%) ranks as the biggest challenge, with 80% of insurers citing churn issues. These challenges have intensified, as insurance interactions are infrequent, making each customer touchpoint critical.

Let’s explore some of these challenges in more detail.

Why Do Brief, Transactional Interactions Hurt Insurance Loyalty?

Little day-to-day contact across digital channels leaves almost no room to build a relationship. Touchpoints are largely limited to renewal and claims, so brand presence fades between those moments.

When customers have little to remember beyond price, a well-timed competitor offer can lure them away with minimal effort.

Our 2025 Loyalty Uncovered Report shows that 85% of insurance companies struggle with customer engagement, making it the sector’s biggest loyalty challenge.

Because contact is so sparse, any friction in a renewal or claims experience carries outsized weight. One negative experience can overshadow months of peace and quiet and erase hard-won retention gains.

The solution is to stay present between formal touchpoints, providing value that keeps your brand front of mind without demanding anything from the customer.

Why Are Trust and Retention Declining in Insurance?

Trust and retention are declining in insurance because providers have so few opportunities to build rapport and demonstrate value outside renewal periods. Without those touchpoints, customers are left wondering whether they are getting their money’s worth.

The data backs this up:

80% of insurers cited churn and retention issues as a major concern.

Only 34% of consumers say they have complete faith in the businesses they patronise.

When trust is low, price becomes the primary decision factor. That is precisely the scenario most insurers want to avoid.

To counter this, improve transparency in the claims experience and communicate proactively across digital channels. Consistent, omnichannel engagement rebuilds credibility and reduces churn.

How Is Regulatory Change Disrupting Insurance Loyalty Strategies?

In the UK, reforms are now disrupting insurance loyalty strategies by removing the pricing tactics insurers have traditionally relied on to acquire and retain customers.

Regulations now prioritise fair value and transparent outcomes, which narrows the room for price-driven approaches and forces a rethink of acquisition, retention, and loyalty economics.

Two reforms stand out:

The FCA’s ban on “price walking” in 2022 eliminated the practice of charging loyal renewers more than new customers. This practice had cost 6 million UK policyholders £1.2 billion in 2018.

The Consumer Duty regulations that came into effect in 2023 further strengthen consumer protection by requiring firms to deliver positive outcomes for retail customers.

These changes protect consumers, but they also force a reset. Unsustainably low introductory deals are no longer viable, so insurers must compete on experience. The days of subsidising aggressive new customer acquisition with loyal customer premiums are over.

What Do Digital-First Customers Expect From Their Insurer?

People want quick, intuitive journeys across digital channels, consistent omnichannel experiences, and personalised experiences that prove value beyond the policy. When those needs go unmet, trust weakens and price sensitivity rises.

Specifically, they expect:

Seamless digital journeys

Personalised communications

Proactive engagement

Value beyond the policy

Transparent pricing and terms

The opportunity for insurers isn’t simply improving renewals or the claims process. You have the chance to upgrade everyday interactions too.

Data analytics and AI can power timely, relevant nudges. Digital self-service can remove friction at every touchpoint. And mapping the full customer journey helps identify where experience is falling short.

Getting this right creates the kind of everyday experience that makes switching feel less worthwhile.

Why Are Insurance Customer Acquisition Costs Rising?

Rising ad bids, tighter regulation, and price comparison dynamics are all pushing the cost of acquiring new customers higher. The same budget simply buys fewer prospects than it did before.

The main cost drivers are:

Agent commissions

Comparison site fees

Onboarding resources

Initial underwriting expenses

Every customer who leaves takes your sunk acquisition cost with them and forces you to spend again to fill the gap. That makes retention one of the most effective levers insurers have.

Better onboarding, proactive engagement, and well-timed cross-selling protect customer lifetime value and reduce churn. The returns add up over time, stabilising unit economics long after the initial marketing spend.

How Do Commoditisation and Price Sensitivity Weaken Insurance Loyalty?

Price comparison sites line policies side by side with prices in bold, and uniform cover descriptions make everything look the same. When offerings feel interchangeable, customers stop engaging, trust stalls, and switching feels low risk.

In that environment, a £20 saving can override years of reliable service. The decision collapses to a single number, and the distinctive value gets buried.

This triggers a spiral as:

Insurers cut costs to stay competitive

Service quality slips and differentiation fades

Weaker experiences push customers to choose on price alone

More churn follows, triggering more cost-cutting

Each stage feeds the next.

Breaking out of it means giving customers something to weigh against that £20 saving: visible value, consistent engagement, and experiences that a price comparison site can’t put in a column.

Why Do Complex Policies and Claims Processes Drive Customers Away?

Complex policies create confusion and friction at the moments that matter most. When customers are unsure what they bought or how to use it, satisfaction drops.

At renewal, that confusion makes price the only thing they feel confident comparing, which raises churn even among long-tenured policyholders.

Drawn-out claims processes add to the problem. The claims process is naturally a high-pressure situation, and unclear steps or slow communication turn what should be a trust-building experience into a liability.

Common pain points include:

Dense documents and jargon

Repetitive documentation requests

Assessor scheduling and coordination

Settlement timing and outcome clarity

The solution is to improve the claims experience with clear expectations, status transparency, and human support at critical stages.

How Are Evolving Customer Expectations Reshaping Insurance Loyalty?

Simple journeys, personalised interactions, and clear value across digital channels are no longer differentiators. They are the minimum. Mobile-first, instant service has shifted from delight to baseline.

Younger policyholders in particular expect digital self-service, always-on support, and transparent pricing and terms.

As these norms spread, yesterday’s innovation quickly feels ordinary. The gap shows up in lower satisfaction and higher churn, especially where claims updates are slow or fragmented.

The brands that keep pace are the ones treating experience improvement as an ongoing discipline.

How Do Legacy Systems and Organisational Silos Undermine Loyalty?

Legacy systems and organisational silos undermine loyalty by preventing customers from getting real-time, unified experiences.

Older technology stacks cannot support personalised interactions, and fragmented teams with limited data sharing slow down decision-making across digital channels.

Customers notice the result: delays, generic messages, and gaps in the claims process that negatively impact satisfaction and increase churn risk.

Without unified data, insurers can’t act on what customers are telling them through their behaviour, their claims history, or their silence. That’s what limits cross-selling, weakens advocacy, and keeps the experience feeling disjointed.

Does Loyalty Really Matter for Insurers?

Yes, it does. Loyalty in insurance is the tendency of policyholders to stay, buy more, and advocate, which drives customer lifetime value and lowers customer churn.

The payoff shows up in two places: bigger revenue per customer over time and a clear cost advantage versus constant acquisition.

How Does Loyalty Boost Customer Lifetime Value?

Loyal customers generate more revenue through tenure and cross-selling. A policyholder who stays with you for ten years might generate 3-4 times the revenue of a one-year customer, even with loyalty discounts factored in.

Predictable, long-term revenue also funds better service, data analytics, and innovation that deepen customer engagement.

Examples of journeys that expand CLV:

A home insurance customer who later adds auto, life, and umbrella policies.

A business client who expands coverage as their company grows.

A health insurance member who upgrades to premium plans as their family expands.

What Is the Cost Advantage of Retention Over Acquisition in Insurance?

Retention is the practice of keeping existing customers, and it is typically cheaper than acquiring new ones. Industry analyses show acquiring a new insurance customer costs 5-9 times more than keeping an existing one.

That gap reflects marketing, commissions, onboarding, and underwriting efforts that repeat with every new customer.

Acquisition vs. Retention Expenses:

Acquisition Expenses

Retention Expenses

Marketing campaigns

Renewal communications

Agent commissions

Loyalty benefits

Underwriting time

Streamlined claim processing

Onboarding support

Self-service tools

Familiar customers already know your processes and trust your brand, which reduces support needs and friction in the claims process.

Clear communications, digital self-service, and well-designed loyalty programmes keep costs down while sustaining satisfaction, advocacy, and long-term customer lifetime value.

What Are the Benefits of Customer Loyalty in the Insurance Industry?

Loyal customers adopt digital self-service, engage more, and churn less. As we’ve seen, the result is stronger customer lifetime value, steadier cash flow, and a brand that wins on trust and reliability rather than price alone.

Let’s take a look at these in closer detail.

How Does Customer Loyalty Improve Insurance Profitability?

Profitability improves as loyal policyholders bundle products, renew reliably, and require fewer incentives. These customers navigate digital channels efficiently and make fewer basic enquiries.

Lower servicing effort, higher tenure, and better cross-selling combine to improve margins while reducing dependence on costly acquisition campaigns and premium discounts to hit growth targets.

Lower servicing costs

Loyal customers use digital self-service more often and need less guidance. Their familiarity with forms and terminology shortens interactions, reduces rework, and frees agents for complex cases.

Over time, operational effort falls and satisfaction improves across renewals and the claims process.

Fewer speculative claims

Long-tenured customers tend to claim only for significant issues. Clear expectations and proactive risk prevention encourage prudent use of cover.

The result is fewer low-value claims, healthier loss ratios, and a smooth claims experience when it matters most.

Streamlined processes

When a customer has been with you for years, their history does a lot of the heavy lifting. Renewals require less paperwork, fewer checks, and cleaner handoffs between underwriting, service, and claims.

Fewer checks, cleaner handoffs, and shorter cycle times follow, reducing escalations and everyday operational friction without any process redesign required.

Predictable cash flow

Consistent renewals and multi-policy relationships stabilise revenue. A dependable customer base lets you plan investments in data analytics, automation, and service improvement.

Fewer billing exceptions and lapses reduce administrative strain and support disciplined pricing decisions.

How Does Loyalty Build Brand Trust and Reputation in Insurance?

Trust grows through consistent outcomes and fair treatment during the claims process. Loyal customers give you room to fix issues and provide candid feedback instead of silently leaving.

Strong retention signals quality to partners and analysts, strengthens reputation across the insurance ecosystem, and makes customers less susceptible to slightly cheaper competitor offers.

Why Are Loyal Customers Easier to Cross-Sell?

Cross-selling potential rises as relationships deepen. Your existing customers convert at 60-70% for additional products versus just 5-20% for new prospects.

You already have the data to personalise recommendations based on their purchase history and behaviour. And because loyal customers trust your brand, they’re far more open to exploring your offers without needing to be convinced from scratch.

How Do Loyal Customers Become Brand Ambassadors?

Advocacy turns satisfied policyholders into a growth channel. Personal recommendations carry more weight than advertising and often bring in people who are already a strong fit for your brand.

Referred customers arrive with built-in confidence and require less persuasion. Word-of-mouth reduces marketing spend while adding pre-qualified prospects, reinforcing a cycle of engagement and retention.

How Do You Build Customer Loyalty in Insurance?

Building customer loyalty in insurance means earning repeat choice and advocacy by delivering value at every touchpoint, from first quote through to renewal and beyond.

The seven steps below turn these principles into practical moves that improve retention and lifetime value.

Step 1: Offer Transparent Pricing

Transparent pricing builds trust from day one. Customers can see exactly what drives their premium and how it changes over time, making them feel informed rather than suspicious. That clarity lowers churn and differentiates you beyond discounts.

To maintain transparency:

Be honest about rating factors. Use interactive tools to show real-time changes as coverage or deductibles shift, and avoid jargon.

Match prices for loyal customers, not just newcomers. Proactively alert existing customers to better rates. The goodwill reduces acquisition costs and lifts customer lifetime value.

Adjust for product price sensitivity. Life insurance customers prize stability, while auto shoppers switch on small savings. Focus on discounting only where it actually improves retention.

Step 2: Deliver Exceptional Product

and Service Quality

Exceptional quality means coverage that adapts to life changes, policies written in plain English, and a claims process that proves your promises. When customers understand their benefits and get help quickly at stressful moments, satisfaction rises, trust deepens, and renewal becomes easier than switching.

Improving service quality often means:

Offering flexible, modular cover. Build products that adapt as needs evolve so customers can add or remove protections without friction. Position yourself as a partner through life events, not a static policy.

Simplifying policy language. Replace jargon with visuals and comparison charts that show what is and is not covered. Clarity cuts confusion and lifts satisfaction.

Making claims your showcase. Provide swift first responses, clear timelines, and proactive updates. A smooth claims process turns a potential low point into a loyalty-building experience, reinforced by useful digital self-service.

Step 3: Build Consistent Trust Relationships

Trust is built through clear advice, honest conversations about what a policy does and does not cover, and a claims process that delivers on its promises. When customers experience that consistency across every channel, renewal becomes the easy choice.

To build these meaningful relationships:

Act as a trusted advisor. Offer timely, practical guidance during life events rather than sales scripts. Help customers choose a cover that fits and shows value beyond the policy.

Be candid about limits. Explain exclusions and trade-offs upfront. Clarity reduces surprises at claim time and prevents the disappointment that erodes trust.

Deliver on claims timelines. Set and meet targets for first contact, assessment, and payment. Train adjusters for empathy and clear updates, turning a stressful moment into a credibility win.

Step 4: Enhance Accessibility and Communication

Customers who can reach you easily and get clear answers stay longer. Make every channel simple to use, strip jargon from every message, and keep people updated throughout the claims process and at renewal.

Tips for effective customer communication:

Offer true multi-channel availability. Keep phone support, add live chat with extended hours, and provide a full-featured mobile app for policy management and claims. Let customers choose their preferred digital channels.

Eliminate jargon in every message. Use plain language and test it with real customers. If they cannot explain it back in their own words, rewrite it.

Send proactive status updates. Automate notifications at key claims milestones to reduce anxiety and inbound contacts. Keep updates short, accurate, and timely so customers never need to chase information.

Step 5: Create Personalised Experiences

Personalised experiences tailor content, timing, and offers to each policyholder’s needs across digital channels, which increases customer engagement and retention.

With our Loyalty Uncovered Report (2025) indicating that 84% of insurance companies plan to invest in personalisation technology, tailored experiences are quickly becoming the industry standard.

Use data analytics and observed customer behaviour to ensure every interaction feels relevant. Here are some other best practices for personalisation:

Trigger communications based on life events. When someone buys a home, suggest relevant cover; when a baby arrives, recommend adjustments.

Let customers set preferences. Give control over frequency and channels to build a sense of partnership.

Base your offers on real data. Use past interactions, claims history, and digital behaviour to propose helpful, specific products.

Step 6: Develop a Loyalty &

Reward Programme

An insurance loyalty programme is a structured way to deliver value beyond the policy through personalised rewards, useful partners, and incentives that keep customers engaged between renewals.

According to our 2025 Loyalty Uncovered Report, strategic brand partnerships are now a top investment priority for 84% of businesses, with insurance companies leading adoption at 86%.

Consider:

Partnerships with complementary businesses for frequent, relevant touchpoints.

Home insurance paired with security systems or maintenance services to reinforce risk prevention.

Auto insurance with preferred repair shops offering priority service and quality assurance.

How should you implement direct financial rewards?

Use clear, repeatable incentives that acknowledge positive behaviour and tenure. Tie rewards to outcomes customers control, and make the redemption straightforward.

The goal is to lift engagement and customer lifetime value while supporting healthier loss ratios. Start with:

Claims-free cashback programmes that reward good risk management and improve loss ratios.

Renewal rebates that return a portion of premiums for loyalty (more effective than upfront discounting).

Milestone rewards that offer special cashback after 5 years, creating specific loyalty targets.

How do lifestyle benefits maintain policyholder engagement?

Offer small, useful perks that fit daily routines, encourage risk prevention, and feel relevant outside a claim or renewal. Delivered through digital channels, these benefits sustain customer engagement, encourage positive behaviour, and make staying feel easier than switching.

Examples of lifestyle rewards include:

Wellness programmes for health insurance customers.

Safe driving apps for auto insurance that gamify responsible behaviour.

Special event access that creates emotional connections beyond transactions.

Premium reductions for gym attendance or home security measures.

How can technology deliver personalised insurance pricing?

Start with clearly permissioned data, simple rules, and visible feedback so that people understand how their actions translate into personalised rewards.

Some of the ways insurers do this include:

Usage-based insurance via telematics that rewards actual safe driving.

Smart home device integration that reduces claims while providing tangible value.

Wearable integration with health insurance that triggers rewards for proactive wellness activities.

How do you give policyholders greater control and flexibility?

Offer simple preferences, modular options, and transparent rules so people feel in charge rather than managed by your processes.

True control and flexibility mean allowing policyholders to shape cover, communications, and rewards to fit their lives. Clear choices boost customer satisfaction and strengthen engagement.

Prioritise the following:

Customisation options that give customers agency in their insurance relationship and align cover with changing needs.

Self-service policy management tools that reduce operational costs while increasing satisfaction and speed.

Opt-in programme structures that let customers choose rewards that matter to them personally for higher ongoing participation.

How do you meaningfully recognise insurance loyalty?

Make appreciation visible and useful, so customers feel valued. Tie gestures to service experience and access, and keep redemption simple through digital self-service.

Small, consistent moments build trust and reliability and reduce the appeal of marginal price savings.

Practical ways to make recognition tangible:

Anniversary acknowledgements and tenure-based status levels.

Priority service with dedicated phone lines for loyal members.

Community building among long-term customers through exclusive forums or events.

Step 7: Measure Impact and Continuously Improve

Go beyond headline retention to understand the quality of relationships and where to act next. Use a simple pattern: gather signal, segment it, act on insights, and close the loop with customers to show progress.

How do you track metrics beyond simple insurance retention?

Track policy persistency ratios, multi-policy households, customer lifetime value, and referral rates. These metrics reveal depth, breadth, and advocacy.

Review them by product and channel to spot where digital self-service, claims process experience, or pricing changes increase engagement and reduce customer churn.

How do you use Net Promoter Score effectively?

Run regular Net Promoter Score surveys and trend them by segment, product, and journey stage. Pair scores with verbatim feedback to find specific solutions.

Follow up with detractors quickly, and share “you said, we did” updates. When NPS moves with a change, you have a credible signal to scale.

What should segmented churn analysis include?

Analyse churn by tenure, policy mix, price sensitivity, and claims history. Quantify full cost: acquisition spend, lost future revenue, and referral drag. Identify patterns you can influence, like first-year lapses after claims decisions or renewal friction, then prioritise actions with the highest financial impact on CLV.

How do you map the insurance customer journey?

Create a journey map that visualises every touchpoint from quote to claim and renewal. Mark pain points, handoffs, and moments that matter, then use customer feedback and operational data to validate.

Fix the weakest link first, because one broken step can outweigh many smooth ones when customers are deciding whether to stay or go.

What Are the Best Practices for a Customer-Centric Loyalty Strategy in Insurance?

The best insurers build loyalty into daily operations. That means clear differentiation, smart use of data and technology, and frontline teams equipped to deliver visible value at every touchpoint.

Here are some of the most effective practices.

Stand Out From the Competition

The insurers that stand out focus on the moments that shape how customers remember them. A fast, fair claims process, proactive guidance, and personalised touchpoints across digital channels build engagement, trust, and brand loyalty.

Our 2025 Loyalty Uncovered Report reveals that 75% of businesses cite market competition as a major challenge, with 33% ranking it as critical to address. Your unique approach to customer relationships can become a competitive advantage when it consistently delivers clarity, speed, and empathy at the moments that matter.

A dedicated claims concierge or a personalised annual coverage review becomes a memorable moment that differentiates your brand. These touchpoints act as your calling card in the market and shift attention from price to service quality and reassurance when customers need it most.

Lean into authentic strengths rather than spreading thin

If you are known for speedy claims, make that the centrepiece. If you excel locally, build community connections that national carriers cannot match. Playing to real advantages feels credible, resonates with customers, and concentrates investment where it delivers distinctive value.

Solve specific pain points better than anyone

If research shows customers hate paperwork, design the simplest documentation process in the industry. Targeted solutions create stories people retell and generate word of mouth that generic improvements rarely achieve.

Implement Customer Feedback

Once you have a clear market position, keep sharpening it with real customer insights. Treat feedback as an operating system: collect it continuously, act on it visibly, and let patterns guide decisions.

This rhythm improves customer satisfaction, reduces churn, and focuses effort on key moments in the claims process and renewals.

Make feedback collection systematic rather than occasional

Run regular pulse surveys, post-interaction ratings, and annual relationship reviews across digital channels. Tag each response to a journey stage so you can spot friction in context.

Pair qualitative comments with Net Promoter Score to see both the “why” and the trend and feed insights straight into your improvement backlog.

The key is closing the feedback loop visibly

When customers suggest improvements, implement changes where possible and tell them what you did. A simple “you said, we did” update builds trust and reliability. Share wins in-app and by email, and route unresolved issues for fast follow-up. Visible action encourages ongoing participation in your feedback systems.

Use feedback patterns to drive strategic decisions

Prioritise themes many customers mention over nice-to-have features. Quantify the impact on churn and customer lifetime value, then fund the highest-leverage fixes first. Build customer advisory panels to test concepts before launch, reduce rework, and avoid costly missteps. Let measured outcomes decide what you scale next.

Build a Complete Insurance Ecosystem

A complete insurance ecosystem connects services, partners, and digital self-service into a single experience that extends value beyond risk protection.

Policy management, claims, and payments sit under one roof, adding everyday relevance that keeps customers engaged, reduces price sensitivity, and makes renewal the path of least resistance.

Start by building outward from the core policy:

Add complementary services with daily relevance (home maintenance, wellness).

Integrate adjacent partners (repair shops, estate planning, home security).

Unite everything in one app or portal for policy, claims, and payments.

Consider subscription bundles that package protections with useful services.

As these pieces connect, the experience starts to feel more seamless. Auto customers move from incident to preferred repair without repeating details. Life customers reach estate resources inside the same app.

Clear journeys, timely updates, and simple choices turn a static policy into a living service, strengthening loyalty across the insurance ecosystem.

Transform Your Agents Into Loyalty Champions

Train your agents to manage relationships, diagnose needs, provide personalised guidance, and maintain proactive communication across digital channels.

Equip them with the right tools and align incentives to retention so everyday interactions lead you closer to your business objectives.

Four shifts are crucial here:

Evolve the role to relationship manager: coach agents to identify needs, guide decisions, and build long-term trust that drives renewals.

Equip with technology and insights: provide a unified customer history, live claims status, and next-best-action prompts from data analytics and artificial intelligence.

Align compensation with retention outcomes: reward policy persistency, multi-policy adoption, referral generation, and first-contact resolution, not just new sales.

Empower the front line to address issues: grant authority to resolve problems, offer small credits, and expedite steps in the claims process without escalation.

Use Technology to Enhance the Customer Experience

Technology should make insurance easy to use, not the other way around. Prioritise digital self-service that removes friction and keep experiences consistent across channels. The goal is a customer who never has to ask, “Why can’t I just do this online?”

Focus on these priorities:

Go mobile first: biometric login, document upload, in-app chat, and quick claims updates.

Offer full self-service portals: policy changes, payments, renewals, and status tracking in one place.

Ensure omnichannel consistency: the same answers across the app, web, phone, and chat to build trust.

Use intelligent routing: send simple queries to digital helpers and complex cases to human experts.

Leverage Data to Power Your Loyalty Strategy

Your customers are already telling you what they need through their behaviour, feedback, and engagement patterns. The challenge is turning that signal into timely action.

84% of insurance companies now prioritise data utilisation for exactly this reason, according to our Loyalty Uncovered Report (2025).

Start with clear questions, collect only what you will use, and connect insights to specific journeys and outcomes.

Here is where to focus:

Start with behaviour-based segmentation: Identify distinct loyalty drivers by group. Young urban renters and suburban homeowners respond to different retention tactics, so tailor messaging, channels, and offers to each segment’s needs and preferences.

Identify what actually drives satisfaction: Pinpoint what matters most to each group and invest in high-impact solutions. Focus budget on the improvements that shift renewal intent rather than broad enhancements that do not move the needle.

Build churn prediction models: Spot at-risk customers early using signals such as reduced engagement, claim outcomes, and price sensitivity. Trigger proactive outreach while relationships are still recoverable.

Anticipate life events for timely outreach: Use existing data to predict moments like marriage, home purchase, or retirement. Engage with relevant guidance and products before competitors appear, reinforcing trust and reliability.

How Do You Measure the Impact of Loyalty in Insurance?

Set clear metrics on day one and review them consistently so improvements are visible and investment decisions are evidence-based. Our research shows that 72% of businesses face scalability issues with their loyalty initiatives, which makes getting this right from the start non-negotiable.

Which KPIs Should You Track for Insurance Loyalty?

The right KPIs go beyond headline retention and reveal the depth, breadth, and momentum of your customer relationships. Focus on metrics that tell you whether people are staying, buying more, and telling others about you. This includes the following:

Policy persistency ratios, multi-policy households, and customer lifetime value.

Referral rates as a signal of advocacy and customer engagement.

Share of wallet to confirm consolidation and trust.

Cross-selling success rates as a proxy for relationship health.

Why Does Net Promoter Score Matter for Insurance Loyalty?

Net Promoter Score is a single-question measure of advocacy that predicts renewal and expansion. Promoters (scoring 9-10) typically stay with insurers 1.8 times longer than detractors and generate more revenue through additional products and referrals.

Track NPS by segment and product to catch issues early. A sudden dip among auto customers may point to pricing pressure or claims handling concerns. Pair scores with verbatim feedback to pinpoint fixes and act on them before the damage compounds.

How Should You Analyse Customer Churn and Retention in Insurance?

Start by segmenting churn by value tiers, tenure, and policy mix to understand the real impact on profitability. Conduct structured exit interviews to uncover drivers beyond price, such as service disappointments or lack of recognition.

The earlier you spot warning signs, the better. Policy downgrades, rising complaints, and missed payments often surface months before cancellation. Calculate true churn cost, including acquisition spend, lost future revenue, and negative word of mouth, to build the business case for focused retention investments.

How Does Customer Journey Mapping Strengthen Insurance Loyalty?

Customer journey mapping visualises the full lifecycle from awareness to renewal across every touchpoint. By plotting each stage and identifying moments of truth, including the claims process, insurers can spot friction before customers feel it, fix the experience where it matters most, and deepen engagement across the entire insurance ecosystem.

The main goals are to surface pain points that hinder satisfaction and to proactively exceed expectations. Implementing the earlier themes, such as aligning internal processes with customer needs, breaking silos, and investing in technology solutions, such as data analytics and digital self-service, will optimise journeys.

Treat mapping as an ongoing process too. Constantly reassess strategies, gather customer feedback, and adapt to changing expectations.

What Future Trends and Innovations Will Shape Insurance Loyalty?

Artificial intelligence is pushing loyalty into a new era of hyper-personalisation. Forward-thinking insurers are already using machine learning to predict needs and trigger timely, helpful moments, and adoption is accelerating.

Our 2025 Loyalty Uncovered Report shows 62% of businesses investing in AI and machine learning, with insurance companies at 63%, slightly above the average.

Behavioural economics is also reshaping programme design. Loss aversion makes status tiers worth keeping. The endowment effect highlights accumulated benefits that people find too valuable to give up. Present bias makes small immediate rewards the gateway to longer-term engagement. These principles align offers with how people actually decide, without relying on constant price cuts.

The advice here is simple: move at a pace that fits your segments and position, but move decisively. Pilot use cases, measure the impact on retention and customer lifetime value, then scale what works. Early movers earn an advantage in data, models, and customer feedback.

The window for clear differentiation is narrowing quickly. You need to choose soon whether you’ll lead or follow.

Start Building Customer Loyalty in the Insurance Industry

Building lasting loyalty means treating every touchpoint as part of a single, designed relationship. Shift from transactional interactions to genuine partnerships that blend clear pricing, simple products, and a dependable claims process.

Design journeys that balance emotion and utility. Pair human reassurance with practical wins: fast first contact on claims, proactive updates, and meaningful, personalised rewards. Use data to time guidance around life events, keep communications jargon-free, and make digital self-service effortless.

Ready to put these strategies into practice? Download our Insurance Retention Action Plan for checklists, templates, and KPIs covering segmentation, journey mapping, NPS cadence, and loyalty programme design.

FAQs

How can insurance companies increase customer loyalty?

Insurance companies can increase customer loyalty by focusing on fair pricing, providing excellent customer service, personalising experiences, offering value-added services, and leveraging technology to create seamless, convenient interactions across all touchpoints.

What role does customer experience play in building loyalty in the insurance industry?

Customer experience plays a vital role in building loyalty in the insurance industry. By delivering seamless, personalised, and hassle-free experiences across all channels, insurers can differentiate themselves and create meaningful connections with customers.

How can data analytics help insurance companies improve customer retention?

Data analytics can help insurance companies improve customer retention by providing valuable insights into customer behaviour, preferences, and needs. Insurers can tailor their products, services, and communications to better resonate with individual customers.

What are some effective strategies for reducing churn rates in the insurance industry?

Effective strategies for reducing churn rates in the insurance industry include proactively monitoring customer engagement, implementing targeted retention campaigns, simplifying complex processes, and offering personalised incentives to at-risk customers.

How can insurance companies leverage digital channels to enhance customer engagement?

Insurance companies can leverage digital channels to enhance customer engagement by developing user-friendly mobile apps, online portals, and chatbots that provide 24/7 access to information and support. Integrating a seamless omnichannel experience makes interacting with your company easier for customers.

What impact can personalisation have on customer loyalty in the insurance industry?

Personalisation can have a significant impact on customer loyalty in the insurance industry. Personalised experiences, such as customised policy recommendations and targeted rewards foster a stronger sense of connection and loyalty.

What role do loyalty programmes play in the insurance industry?

Loyalty programmes play a crucial role in the insurance industry by incentivising repeat business, encouraging customer engagement, and strengthening relationships. Relevant, personalised rewards based on customer preferences and behaviour improve value perception that also drives long term advocacy.

What are the benefits of building strong customer loyalty in the insurance industry?

Strong customer loyalty offers numerous benefits, including increased customer retention, higher lifetime value, reduced acquisition costs, and positive word-of-mouth referrals. Loyal customers are more likely to purchase additional products, provide valuable feedback, and endorse the brand.

Mark Camp

Mark is the Founder and CEO of Propello Cloud, an innovative SaaS platform for loyalty and customer engagement. With over 20 years of marketing experience, he is passionate about helping brands boost retention and acquisition with scalable loyalty solutions.

Mark is an expert in loyalty and engagement strategy, having worked with major enterprise clients across industries to drive growth through rewards programmes. He leads Propello Cloud’s mission to deliver versatile platforms that help organisations attract, engage and retain customers.

Start your customised Propello Cloud journey today

Explore the platform’s scalability, features and customisation options and get answers to your unique questions.